On 11 November 2024, the Federal Tax Authority (“FTA”) published the Corporate Tax (“CT”) return guide to assist taxpayers with the preparation of their first UAE CT return. The UAE CT return guide provides extensive details on how the CT return will operate, how the forms, calculations and schedules are designed, what elections are available to taxpayers in certain cases and the interplay between the different sections, amongst other things.

It also details the information needed for transfer pricing (“TP”) disclosures, including transactions with related parties and Connected Persons. This includes specific guidance on qualifying thresholds for aggregate values of related party transactions, reporting payments to Connected Persons, and instructions on reporting gains/losses from asset transfers and adjustments for non-arm’s length transactions. However, it is worth noting that not all data fields will be relevant to every taxpayer.

Key Next Steps

Identify the required data points to complete the CT return, as the return consists of a total of 20 additional tax schedules that could be applicable depending on your tax profile. This will require many granular level data points which would not typically be obtained at General Ledger (“GL”) account level and may not be easily accessible for Tax teams (for example HR employee data).

Ensure to be ready to make your tax elections, which must be made in the first tax period and will be considered final (except for the foreign Permanent Establishment (“PE”) election).

Consider the need for a technology solution that can help (automatically) maintain and govern the required tax schedules.

Complete your transfer pricing assessment before the relevant financial accounts are closed to minimize the need for downward TP adjustments that require FTA approval.

We recommend all taxpayers to review their information on the EmaraTax portal to ensure that it is complete and accurate. If this is accomplished, no irrelevant or incorrect schedules may need to be completed as part of the CT return filing process. There is a grace period (ending 31 March 2025) in which taxpayers can update their information on the EmaraTax portal without incurring penalties.

In this alert, we have summarized information from the CT return guide by topic.

Documents required to be submitted alongside UAE CT return

Financial statements (audited or unaudited) must be submitted alongside the UAE CT return. If the taxpayer has prepared audited financial statements, they will be required to disclose the name of their auditors and the audit opinion provided.

However, taxpayers have the option to submit the following documents where applicable:

Documentation to support the market value of qualifying financial assets and liabilities where the election is made under the transitional rules.

Tax residency certificate to support tax residency status in a foreign jurisdiction under a double taxation agreement.

Evidence of foreign tax paid in a foreign jurisdiction when claiming a foreign tax credit in the CT return.

Accounting information

All taxpayers will be required to provide a breakdown of their financial statements (income statement, statement of financial position and statement of other comprehensive income) prepared under IFRS or IFRS for SMEs. The information should be provided on a standalone basis, except where taxpayers are part of a tax group.

Taxpayers who use the cash basis of accounting will only be required to disclose information on the income statement.

Taxpayers who need to convert the currency of their financial statements into AED must use the rates set by the Central Bank of UAE.

Tax elections

Most tax elections must be made in the taxpayer’s first tax period, except for the foreign Permanent Establishment (“PE”) election, which can be made on an annual basis.

Any election made in a CT return will be considered finalon submission of the CT return. The FTA will not send the taxpayer any confirmation letter. Where an election applies to future tax periods, it will automatically be reflected in future CT returns.

Where the realization basis has been elected and the taxpayer receives approval from the FTA to revoke a previous election, the taxpayer will not be able to make another election in a future tax period.

Transitional rules:

Businesses electing to apply one of the transitional adjustments relating to qualifying immovable property, qualifying intangible assets or qualifying financial assets and liabilities in their first tax period will be required to complete the relevant tax schedules in the CT return regardless of whether the asset and/ or liability was disposed of in the tax period. However, an adjustment will only be made in the tax computation in the tax period in which the actual disposal takes place.

Certain fields will require careful consideration if the taxpayer is a tax group or a member of a qualifying group, these fields include but are not limited to

date of ownership;

original cost and net book value prior to/ at the start of the first tax period; and

the market value of the relevant qualifying asset / liability at the start of the first tax period.

A different treatment will apply to members of a tax group. For example, if none of the members of the tax group were subject to UAE CT before the creation of the tax group, then an election can be made in the first tax period of the tax group. In this scenario, if a member leaves the tax group or the tax group ceases to exist, the taxpayer will be required to follow the same election that was applied to the tax group.

However, if any members first tax period has passed before joining the tax group, any previous elections made in relation to certain assets will continue to apply only to such assets in the tax group. In this scenario, if a member leaves the tax group or the tax group ceases to exist, the taxpayer will be required to follow the same election that was applied previously before the entity joined the tax group.

Foreign PE election:

Taxpayers will be required to disclose information regarding their eligible and non-eligible foreign PEs. Eligible foreign PEs are those that are subject to tax at a rate of at least 9% in the foreign jurisdiction.

The tax schedule will not calculate the income and expenditure attributable to the foreign PEs, however the schedule will track income and expenditure attributable to such PEs as well as the amount of the tax loss attributable to the foreign PEs (including how much of these tax losses were offset against taxable income in prior tax periods).

For non-eligible foreign PEs, the name and jurisdiction are to be provided.

Qualifying Free Zone Persons (“QFZP”)

Where a QFZP has opted out of the Free Zone (“FZ”) regime, the UAE CT return will not provide the QFZP fields in the current and subsequent four tax periods.

QFZPs will be required to disclose information regarding the level of substance maintained in the FZ and provide confirmations that they meet all the conditions to be a QFZP (including TP requirements).

In particular, the QFZP, will need to disclose the total average number of full-time employees including the average number of full-time employees located in the FZ, all operating and capital expenditure incurred in deriving qualifying income. Where the core-income generating activities have been outsourced to an external service provider, details need to be included in the UAE CT return such as name of outsourcing provider, address, corporate tax registration number, total expenditure spent on the outsourcing provider in the tax period, the average number of full time employees provided by the outsourcing provider and confirmation that adequate supervision has been provided by the taxpayer on the activities that have been outsourced.

Tax Reliefs

Transfers within a Qualifying Group Schedule:

Where the taxpayer has elected to benefit from relief under the transfers within a qualifying group provisions in the current or prior tax period, both the transferor and transferee will be required to complete this schedule. The schedule should also be completed by both the transferor and transferee when the 2 year clawback provision of Article 26 of the UAE CT Law is triggered in the current tax period.

Certain fields will only be available to the transferor in the schedule such as net book value of the asset or liability at the date of transfer, date of the transfer (consistent with the date recognised in the financial statements), and whether a gain or loss has arisen on the transaction.

Where the clawback provisions have been triggered, the transferor and transferee will be required to provide details in relation to the transaction counterparty name and CT TRN, whether the taxpayer was the transferor or transferee when the transaction took place, and whether the transferor is still a taxpayer. They will also be required to provide the market value of the asset or liability when the transfer took place, along with the date of the original transfer and adjust for the amount of gain or loss that was initially exempt from UAE CT. This adjustment will only be recognised in the transferee’s taxable income calculation if the transferor has ceased to exist.

Business Restructuring Relief Schedule:

Where the taxpayer has elected to apply business restructuring relief, both the transferor and transferee will be required to complete this schedule. The schedule should also be completed by both the transferor and transferee when the 2 year clawback provision of Article 27 of the UAE CT Law is triggered in the current tax period.

Certain fields will only be available to the transferor in the schedule such as net book value of the assets and/ or liabilities of the business at the date of transfer, date of the transfer (consistent with the date recognised in the financial statements), whether a gain or loss has arisen on the transaction.

Where the clawback provisions have been triggered, the transferor and transferee will be required to provide details in relation to the transaction counterparty name and CT TRN, whether the taxpayer was the transferor or transferee when the transaction took place, and whether the transferor is still a taxpayer or natural person. They will also be required to provide the market value of the assets and/or liabilities of the business when the transfer took place, along with the date of the original transfer and adjust for the amount of gain or loss that was initially exempt from UAE CT. This adjustment will only be recognised in the transferee’s taxable income calculation if the transferor has ceased to exist or the transferor is a natural person.

Interest deduction limitations

Taxpayers will be required to calculate the net interest expenditure under the general interest deduction limitation rule in the current period before completing the interest capping schedule. The schedule will only calculate the amount of net interest expenditure that is tax deductible.

If a member of a tax group is a bank or insurance provider, the net interest expenditure attributable to that member should be excluded from the interest capping schedule.

The schedule includes separate sections for non-deductible net interest expenditure relating to a single entity or a tax group. Adjustments can be made to adjust the disallowed net interest expenditure however a reason needs to be provided to explain the adjustment taken. The schedule will also track any pre-grouping net interest expenditure brought forward, as well as any disallowed pre-grouping net interest expenditure brought into the tax group by a new subsidiary. Tax groups will be able to choose in a tax period whether they wish to utilise pre-grouping net interest expenditure attributable to a subsidiary. Where a tax group has unutilised net interest expenditure and its members have pre-grouping net interest expenditure, the net interest expenditure should be utilised in the order in which the amount was incurred.

The schedule will also require taxpayers to disclose any disallowed net interest expenditure that has expired (i.e. the 10-year time limit to carry forward the amount has lapsed).

Tax losses

The UAE CT return has two different schedules in relation to tax losses: one for tax standalone taxpayers and another for tax groups.

Most of the information relating to tax losses will be pre-populated in the CT return. However, certain information will require manual inputs, for example where tax losses have been transferred or received as part of Business Restructuring Relief or where the tax losses have been limited as a result of the change in ownership and change in business activity provisions.

There are two input fields to respectively manually increase and decrease the amount of the tax losses. The input fields can be utilised, for example where the taxpayer is listed on a recognized stock exchange or where the taxpayer is a natural person (no tax loss restrictions apply in these cases). If one or two of these input fields is used, the reason for adjusting the tax losses will need to be provided in a separate input field.

In addition, the tax group tax loss schedule will have specific sections where the taxpayer will be required to disclose information regarding losses attributable to new and existing subsidiaries and disclose any pre-grouping tax losses. These tax losses can be adjusted in certain situations, for example where a subsidiary leaves the tax group and any remaining pre-grouping tax losses will follow the company.

Foreign tax credits

Taxpayers seeking to claim a foreign tax credit against their UAE CT liability will be required to complete the foreign tax schedule. The schedule will calculate the foreign tax credit available and taxpayers will be required to provide the following information in the CT return:

Name of the foreign country, taxable income attributable to that country, the tax liability in that country, confirmation evidencing the quantum of the tax liability in the foreign jurisdiction (e.g. certificate of deduction of withholding tax), nature of the tax credit (e.g. tax type and what income was subject to tax) and amount of UAE CT due on the relevant income (after application of the exemption, the 0% rate or utilisation of tax losses). Documentary evidence must be provided.

If a UAE CT group is claiming the foreign tax credit, the foreign tax credit is claimed at (and needs to be allocated to) the specific member of the CT group that has received the relevant foreign source income. The foreign tax credit amount will reduce the CT payable at the tax group level.

Additional disclosure requirements

UAE Dividends schedule: taxpayers will be required to disclose details about dividends and profits distributions received from resident persons subject to UAE CT. There is no requirement to disclose dividends and profit distributions received from exempt companies.

Participation Exemption schedule: taxpayers will be required to complete this schedule if they have derived income or losses from a participation during the tax period and must confirm that all the conditions to receive the exemption are met. For example, confirming that the participation is subject to CT at a rate of at least 9% and the ownership requirements are met. Based on the information provided, the CT return will calculate the adjustment required to taxable income.

The CT return includes an additional schedule for income and losses that are not recognised in the income statement. If an amount relates to unrealised gains or losses (which will not be subsequently recognised in the income statement) and where an election has been made to apply the realisation basis, the amount should not be included in the UAE CT return.

Taxpayers will be required to complete unrealised gains / losses schedule if they have elected to apply the realisation basis and have unrealised gains or losses arising in the tax period. When a gain or loss has been realised, the taxpayer must complete the deferred gains or losses schedule.

Miscellaneous administrative guidance

Where the taxpayer falls outside of the scope of CT by virtue of a double taxation agreement, the taxpayer will not be required to submit a full CT return.

If the taxpayer becomes aware that a CT return previously submitted to the FTA or a tax assessment issued by the FTA is incorrect and the error increases the CT payable up to AED 10k, the FTA will allow the taxpayer to correct the error in the CT return that is not due for submission for a previous tax period or in the CT return for the period in which the error has been discovered, whichever is earlier.

If the CT payable is higher than AED 10k, the taxpayer will be required to submit a voluntary disclosure.

Taxpayers who have completed the CT return using estimated financial data, will be required to disclose and declare that the data provided are estimated figures and not final figures.

Exempt businesses including qualifying public benefit entities, pension or social security funds, qualifying investment funds, and entities wholly owned and controlled by certain exempt businesses will not be required to prepare and submit a CT return. Instead they will be required to make an annual declaration confirming that they meet all the conditions to be exempt from UAE CT.

However, if an entity ceases to be an exempt business for UAE CT and becomes a taxpayer, i.e. subject to tax, the entity must submit a CT return for that relevant tax period.

Transfer pricing

Thresholds – what is in, what is out?

Taxpayers with an aggregate related party transaction value of AED 40m either recorded in the financial statements or at market value, are required to prepare and file a disclosure form along with the CT return. Once this initial criterion is met, the threshold for reporting individual transaction types is AED 4m.[1]

But there is potentially a catch:

The CT return guide defines ‘financial statements’ as:

‘A complete set of statements as specified under the Accounting Standards applied by the Taxable Person, which includes, but is not limited to, statement of income, statement of other comprehensive income, balance sheet, statement of changes in equity and cash flow statement.’

As such, an objective interpretation of the above definition could imply that related party transactions with a balance sheet impact should be included when assessing the AED 40m qualifying threshold.

However, such a position could potentially lead to several unique scenarios and potentially unintended outcomes (e.g., interest-bearing loans, accounts receivable / accounts payable balances, etc.) that require further analysis and clarification from the FTA in terms of their treatment. More importantly, taxpayers should plan ahead and review their related party transactions carefully to assess whether they meet the qualifying threshold.

[1] Dividends between related parties do not need to be disclosed and should not be considered in determining the AED 40m or AED 4m thresholds.

Adjustments

Another unique aspect of the UAE TP disclosure form is the distinction between gross transaction value and arm’s length transaction value. Taxpayers need to report both values independently, and the difference between them is automatically reported as an adjustment, as opposed to reporting the net impact.

Further, the FTA’s position on ‘downward adjustments’ is clear, in that any adjustments to non-arm’s length transactions resulting in a decrease in taxable income must be reported to and approved by the FTA prior to submission. Taxpayers should therefore proactively monitor their year-end TP outcomes:

to minimize any deviations from the arm’s length standard in the first instance; or

if a deviation exists, identify it in advance of finalizing their financial statements to report adjustments correctly in the disclosure form.

It is important to note, that the aggregate value of all adjustments (reported under ‘Other adjustments’) should be equal to or more than the aggregate value of all adjustments reported in the disclosure form (i.e., in the related party transactions and Connected Persons schedules respectively).

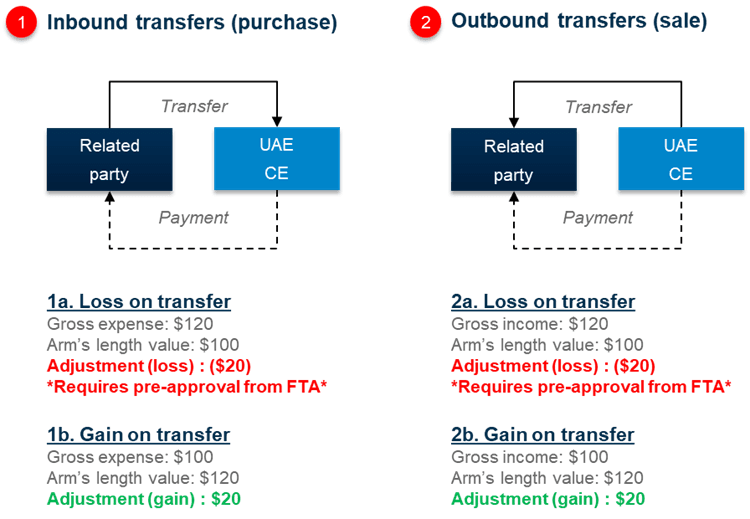

Gains and losses

Taxpayers must also report realised gains or losses (in the current tax period) on prior related party transfers of assets or liabilities, relative to the market value of those transactions. The illustration below summarizes both scenarios.

Taxpayers should carefully evaluate deviations from market value arising during the transfer of assets or liabilities, well before finalizing their financial statements, to ensure accurate reporting in disclosure form. In particular, the focus should be on scenarios 1a. and 2a. above, which will require pre-approval from the FTA. We expect the FTA to release further guidance on the approval pre-process over the coming months.

Connected persons

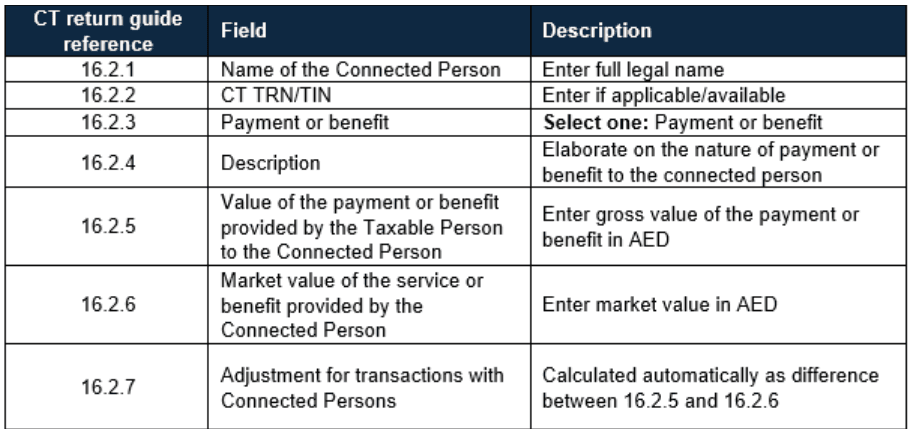

Payments or benefits provided to at least one Connected Person, whose aggregate value exceeds AED 500k must be reported in the disclosure form. Adjustments work in a comparable way to other related party transactions. It is important to determine the arm’s length nature of payments or benefits to Connected Persons, and this requires a review from a corporate tax, transfer pricing and reward perspective.

Disclosure form schedule

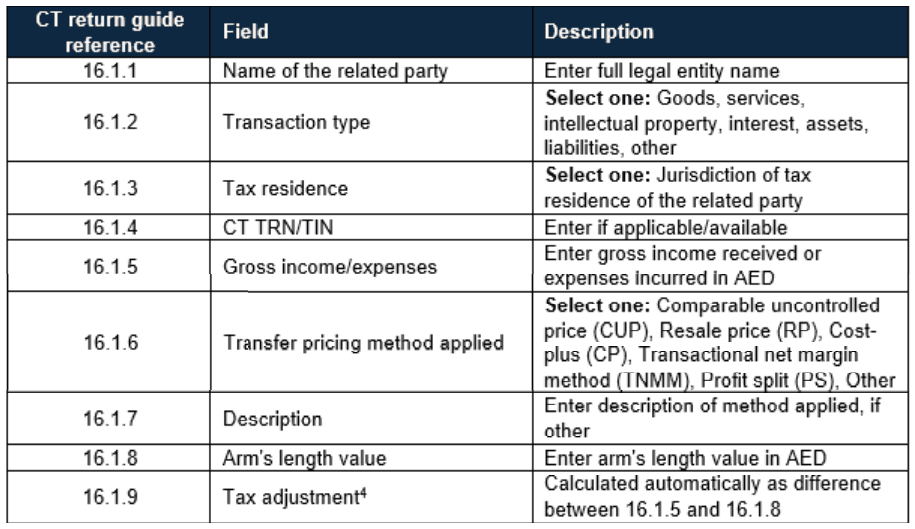

[2] The guidance does not include an official template but does provide information on all required fields in the related party transactions and Connected Person schedules, as summarised below.

Related party transactions schedule

[3] Please note that this our preliminary view based on available information and is likely to be revised as more guidance and clarifications from FTA are published.

[4] Negative or downward adjustments must be pre-approved by the FTA.

Connected Persons schedule

Key takeaways

The CT return guide is an important development which provides taxpayers with certainty on critical elements of the UAE tax compliance process, highlighting the numerous underlying data points required. While many taxpayers have focused on tax sensitization of their General Ledgers (“GL”), this was merely the beginning. The guide indicates that up to 20 schedules may need to be completed, depending on each taxpayer’s tax footprint. Many of these schedules require data points not typically captured at the GL account level. Additionally, tax teams may not even have direct access to these data points and will rely on other departments to provide this information accurately and on time.

Examples of such data include employment information, detailed breakdowns of related party transactions by type (if thresholds are exceeded), aggregate values of transactions with Connected Persons (if thresholds are exceeded), and UAE dividends received per distribution company.

Technology can significantly streamline the maintenance of certain schedules, making the process more automated and efficient. For instance, the tax loss schedule can be largely automated with the right technology, allowing software to track tax losses and their utilisation over time.

Moreover, technology can enhance the governance of your CT return preparation, including schedules, by accommodating data uploads in set formats, storing attachments, maintaining notes, and tracking changes. Selecting the appropriate technology for your tax provisioning and CT compliance processes will not only help you stay in control of your UAE CT compliance obligations but will also help building a robust audit defense file, ensuring readiness for future audits.

From a transfer pricing perspective, taxpayers should adopt a cautious approach and evaluate all related party transactions, regardless of which financial statements are impacted (i.e., income statement or balance sheet) to assess whether they meet the qualifying threshold of AED 40m. We expect further clarifications from the FTA on this critical and relevant point.

The requirement to report adjustments to non-arm’s length transactions, and reporting gains or losses on related party transfers of assets or liabilities are unique to the UAE TP guidelines and will require taxpayers to undertake additional due diligence for accurate reporting. Considering these developments, it is imperative for taxpayers to have a good handle on their TP arrangements to ensure that:

There is a robust assessment of all related party and Connected Persons transactions and whether they satisfy the AED 40m or AED 500k qualifying thresholds;

Related party transactions and their compliance with the arm’s length principle should be thoroughly validated; and

Any subsequent adjustments arising due to non-arm’s length pricing or gains/losses from transfers are quantified and accurately recorded in the financial statements prior to finalization.

HOW CAN DSU HELP?

The UAE CT return guide provides a comprehensive overview of UAE CT return filing requirements and includes extensive information that taxpayers need to review and interpret to effectively to successfully complete their first CT return.

Taxpayers can now proactively plan their compliance lifecycle, assessing readiness for preparing financial statements, completing the UAE CT return, and addressing TP policies, related-party transactions, and pricing – all well in advance of the compliance deadlines.

As the first year of formal CT and TP compliance in the UAE – we understand this is uncharted territory for taxpayers and we’re here to help. In particular, we can support with the following:

Data readiness for UAE CT and TP compliance;

TP impact assessment and policy design;

Tax provisioning support for financial reporting purposes;